Affordable Care Act Enrollment in New Hampshire 2026: What Happened, What It Means, and What Comes Next

Source: Wall Street Journal

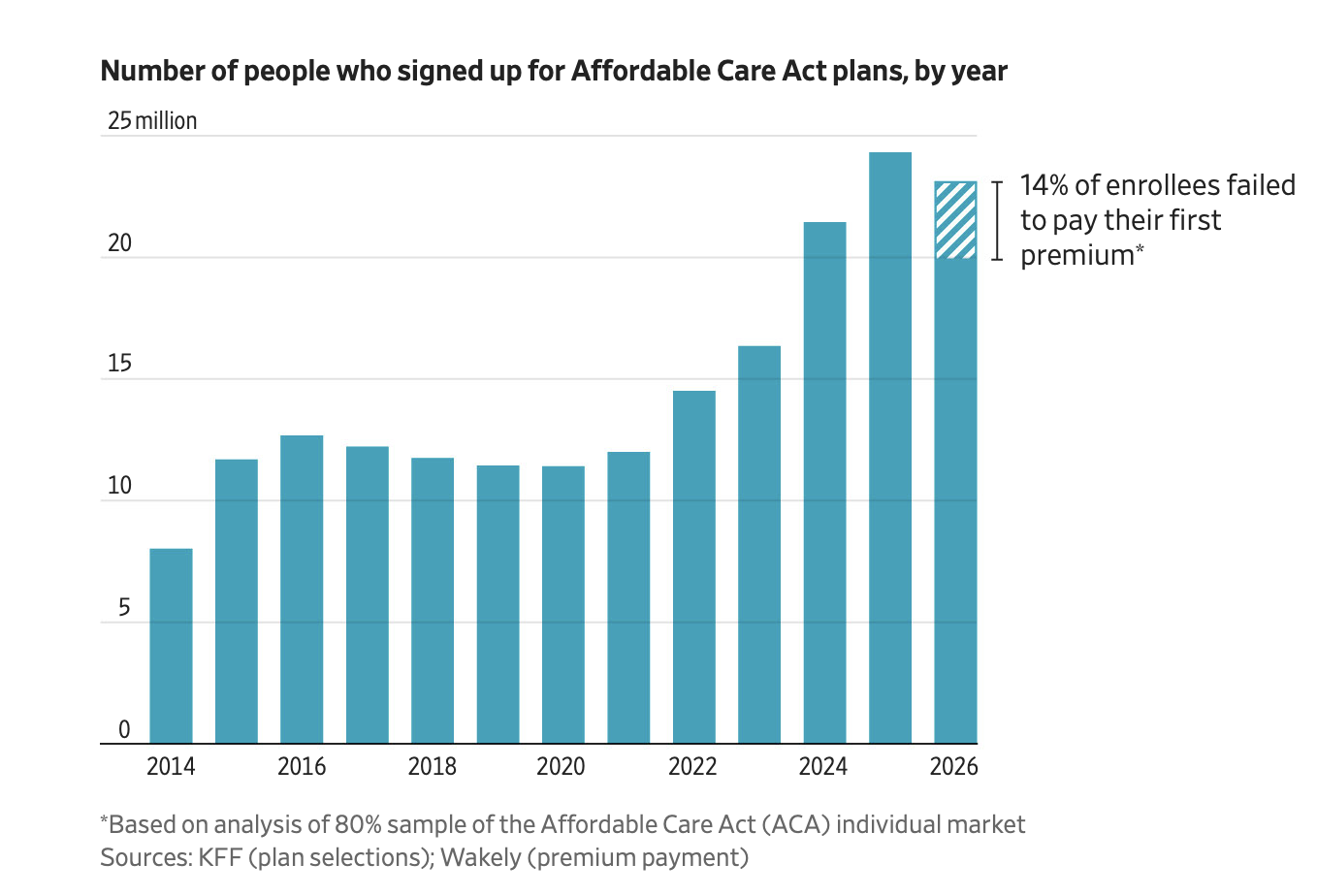

After reaching a record high in 2025, Affordable Care Act enrollment is now dropping sharply across the country, and new national reporting suggests the decline may be deeper than some policymakers first expected. According to a recent report in The New York Times, millions of Americans are dropping ACA coverage following the expiration of enhanced federal tax credits that had made marketplace plans significantly more affordable in recent years. Early federal enrollment figures already showed more than one million fewer Americans signing up for 2026 coverage compared to 2025, but insurers and analysts now believe the actual losses will grow substantially as consumers struggle to afford higher monthly premiums and drop their ACA plans.

These new data paint a troubling picture. Nationally, roughly one in seven people who initially enrolled in ACA plans for 2026 failed to pay their first premiums, according to new actuarial analysis cited by The Wall Street Journal, an unusually steep drop-off compared to prior years. Analysts now estimate total ACA enrollment could decline by as much as 26 percent before the end of the year as rising premiums force families to downgrade coverage, switch to less comprehensive plans, or leave the market entirely.

New Hampshire is experiencing those same pressures. Earlier enrollment data showed the state’s ACA marketplace enrollment declining 6.1 percent, falling from 70,337 enrollees in 2025 to 66,024 in 2026, with more than 4,200 Granite Staters leaving the program year over year. And that only represents the beginning of the decline, as national nonpayment trends will also play out locally.

Against that backdrop, New Hampshire’s latest enrollment experience tells a story that is both concerning and, in some ways, more stable than what is unfolding nationally. While any decline in coverage raises serious concerns for families, providers, and the broader health care system, New Hampshire’s enrollment losses so far appear somewhat smaller than those seen in many other states. At the same time, the data raise important questions about whether more could have been done to help residents maintain affordable coverage during a year of rapidly rising costs and growing uncertainty.

A clearer picture of enrollment declines will emerge later this year, when more comprehensive state-by-state data are released. But if New Hampshire follows the broader national trend, and roughly one in seven enrollees ultimately drops coverage due to nonpayment, the state could see more than 10,000 additional residents lose or drop insurance before the year is over. And, that is not counting anticipated Medicaid enrollment losses. Understanding why enrollment is falling and what comes next will be critical not only for public health, but also for household financial stability, provider sustainability, and the long-term health of New Hampshire’s insurance market and our economy.

A Step Backwards After Historic Gains

The latest decline comes after several years of steady growth in ACA enrollment. Enhanced federal premium tax credits, expanded outreach, and rising awareness pushed New Hampshire’s insured rate to a record high in 2025.

Those gains were built over more than a decade and will not disappear overnight—but 2026 represents a turning point toward a worrisome enrollment decline.

As premiums rose sharply leading into 2026, outreach efforts like patient navigators and enrollment counselors were mostly eliminated. New Hampshire, which relies on the federal marketplace, felt these pressures directly. For residents who purchase their own health insurance, the ACA remains one of the most important pathways to coverage. But this year’s enrollment season came with a harder reality: coverage is still available, yet for many people it now costs significantly more; and for thousands of others, coverage is financially out of reach altogether.

What Comes Next

For New Hampshire, much will depend on future policy decisions, affordability trends, and whether additional steps are taken to stabilize coverage and provide consumer assistance. A deeper look into the factors driving affordability, access and enrollment is important to inform next steps.

Program Cuts from Washington and Inaction at Home

Several forces converged during the enrollment cycle that should be noted. These trends help explain what we are now seeing in both national and state-level data.

Federal subsidy uncertainty. Congress failed to permanently extend the enhanced ACA tax credits that had made coverage affordable for tens of thousands of New Hampshire residents since 2021. As a result, insurers priced 2026 plans assuming those subsidies would expire, contributing to higher premiums.

Mariana Poore served as Coordinator of Health Insurance Navigation at the Foundation for Healthy Communities during the latest enrollment cycle. She stated these financial pressures landed unevenly on consumers. “With the expiration of premium tax credits, some people faced dramatic shifts,” she noted. “One young woman I worked with went from paying $20 a month last year to $101 this year on the same income.”

Premium pressure. Insurers across the Northeast imposed significant rate increases, driven by hospital consolidation, rising pharmaceutical costs, workforce shortages, and higher utilization post-pandemic. For many families, sticker shock alone was enough to abandon enrollment.

“People were questioning whether they could afford to stay in the marketplace at all,” Poore shared. “Families moved from gold plans to bronze plans just to keep something, and we don’t know how many will continue to afford the plans they signed up for throughout the year.”

The highest premium increases for 2026 were faced by older adults (age 50-64). More than 50% of all enrollees who lost eligibility for tax subsidies were in this age bracket. Many older enrollees were already in the lowest-cost bronze plans and had no cheaper options to step down to.

Navigator/Consumer Assistance cuts. At the same time that subsidies expired, the federal government slashed funding for ACA Navigators by nearly 90 percent. In New Hampshire, that meant the loss of most local, in-person enrollment assistance—these cuts were especially damaging in rural areas and for residents with limited internet access or language barriers.

“We had hired a team of six navigators for the cycle. Then we found out that 92% of our funding had been cut, and went from six navigators to one,” recalled Poore. “The remaining 8% was directed to the call center, and I had to recertify as an application counselor to keep supporting people.”

State Inaction. Unlike some states that stepped in with bridge funding, supplemental outreach, or state-based affordability programs, New Hampshire offered no new state resources and pretty much directed consumers to rely on community organizations to fill the gaps. Without state investment in consumer assistance or patient navigators to meet the need, the downsized program that Poore coordinated had limited reach. Moreover, that program has now expired altogether and is no longer available to consumers in need of future enrollment support.

What Other States Did to Maintain Affordability and Protect Coverage

Several states adopted state-level strategies that helped cushion the blow for their residents. These investments and policy interventions include:

State-Based Marketplace Subsidies and Special Enrollment Periods

States that operate their own ACA marketplaces—known as State-Based Marketplaces (SBMs)—had more flexibility to tailor enrollment outreach, extend deadlines, and design targeted plans for their residents.

Some moved proactively to mitigate the impact of federal subsidy cuts. Connecticut launched a special enrollment period with new state subsidies targeting households affected by the loss of enhanced federal tax credits. Backed by roughly $70 million in state funds, the initiative allows eligible residents to receive state-supported premium credits that partially replace the lost federal assistance and stabilize premiums. Other examples include California’s Covered California and Colorado’s marketplace - states that were monitoring enrollment trends in real time rather than relying solely on the federal platform.

In total, 10 states and the District of Columbia offered state-based premium assistance or cost-sharing reductions to supplement or replace the federal tax credits that expired at the end of 2025. These initiatives were aimed at preventing massive premium hikes for residents in state-run marketplaces. Even modest state-level investments and strategies in SBM states have helped retain people with coverage during policy uncertainty.

Expanded Outreach and Extended Deadlines

In Pennsylvania, community health advocates and state insurance officials worked together to extend the open enrollment deadline and to highlight enrollment through events and local forums—an example of how state agency outreach campaigns and partnerships with advocacy organizations can support enrollment despite federal challenges.

Who Is Most Likely to Lose Coverage?

Low- and moderate-income individuals were most likely to drop health insurance as costs rise, and particularly younger adults ages 19–44. The end of pandemic-era Medicaid continuous enrollment has already pushed millions off Medicaid and is expected to continue affecting ACA coverage rates.

Younger adults, healthier individuals without ongoing medical needs, and people seeking lower-cost or catastrophic plans are more likely to opt out when affordability declines. Coverage losses also disproportionately affect communities of color, including Latino adults, who already face higher uninsured rates.

The disability community is among the most vulnerable to coverage instability. Lisa Beaudoin, Principal Consultant of Strategies for Disability Equity, described how families have been affected:

“The paperwork burden on caregivers is enormous, meaning that people with disabilities can end up uncovered for weeks or months at a time. Losing coverage even briefly can threaten their health and continuity of care,” Beaudion shared. This is true for both Medicaid and the Health Insurance Marketplace.

Where New Hampshire Did Better Than Many States

Despite these challenges, New Hampshire’s ACA enrollment had some notable results:

The state still maintains one of the lowest uninsured rates in the country,

Most residents who lost coverage did so due to cost and complexity, not eligibility,

The marketplace itself remained stable, with insurer participation intact.

These are signs of a system under strain. Many recent studies show that access and affordability are still real barriers, even for those with insurance. Co-pays and high deductibles mean that even those with insurance struggle to pay for care in New Hampshire - basically, health insurance is not enough to feel health security anymore.

Where We Go From Here

The takeaway for 2026 is fairly stark: the ACA is still essential, but it has become harder for many people to benefit as intended. The law continues to provide a critical pathway to coverage, especially for people who do not get insurance through an employer. But with enhanced subsidies gone, the Marketplace is expecting that individuals and families will absorb much more of the cost themselves. That means enrollment assistance matters even more as costs soar, and plan selection can make the difference between staying covered and going uninsured. In other words, the ACA remains a lifeline in 2026, but for many households it is now a more expensive and more fragile one.

New Hampshire entered 2026 from a position of relative strength—but will need state policy attention to achieve resilience in the Marketplace.

The early decline in enrollment reflects real pressures on families navigating rising costs, fewer supports, and growing uncertainty. If those pressures continue unaddressed, January’s drop in coverage will hit double-digits in the Granite State before the end of the year. The 2026 enrollment numbers should be read as a warning, but not a final verdict.

There are clear paths forward:

Restoring navigator funding—or replacing it with state funding sources—would help ensure access is informed, equitable, and not dependent on ZIP code or digital literacy.

State leadership and investment could play a stronger role in outreach, education, and consumer protection as costs continue to rise.

Federal action to renew enhanced premium tax credits would immediately improve affordability.

Most importantly, coverage must be treated as what it is: a foundation for economic stability, workforce participation, and community health.

“The negative downstream effects of losing coverage cost far more than maintaining it,” Beaudoin warned.

Health Insurance enrollment through the Affordable Care Act remains one of the most powerful public health tools we have. Protecting it—and the people who rely on it—will require action, coordination, and renewed political will in the year ahead.